.

The announcement of Budget 2020 was awaited with bated breath, post last years’ Corporate Tax rate cut. The Finance Bill 2020 has proposed several sweeping changes in personal taxation, which will impact individuals, organisations as well as Non-resident assesses. The following are important announcements / proposed changes made this year, which would be of interest to the readers:

NRI Taxation: The requisite period a person needs to stay out of India to qualify as a Non-Resident Indian (NRI) has been extended from 182 days to 242 days. Also, Indian citizens who aren’t liable to pay taxes abroad, will be regarded as Indian Residents and will be liable to pay taxes in India, on their global income. The intent is to get in tax net ‘stateless persons’ who don’t pay tax in any country but are citizens of India. They abuse the law by shifting their stay in no-tax jurisdiction to avoid payment of tax in India. This provision was wrongly interpreted that even those Indians who are bonafide workers in other countries, like UAE, where there is no tax on individual incomes earned, would have to pay tax on income earned there. However, the Finance Ministry clarified that such persons will not be taxed.

Abolition Of DDT: In India, companies declaring dividend, pay effective rate of 20.5% as Dividend Distribution Tax (DDT), over and above the Corporate Tax paid on profits. Removal of DDT makes the tax system fair. Now on, Dividends declared and paid by the Companies or Mutual Funds, will reach investors without any deduction of DDT. They will be taxed in hands of investors according to their Tax slabs. Investors with lower or no Tax liability will pay lower tax than 20.5% DDT which was deducted earlier. This rule negatively impacts people in higher Tax slabs (30% and above) as they will now pay higher taxes for dividends received.

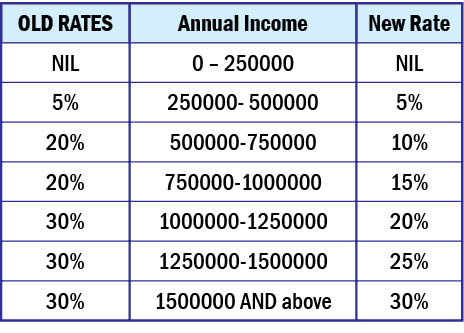

Changes In Personal Tax Rate: This budget has introduced three new slabs offering tax-payers the liberty to choose the most beneficial system for them. However in India, where there is no social security and one has to pay for his own medical cover, by removing tax incentives on section 80C investments and Mediclaim premium, which are mainly retirement saving avenues and medical cover, it can be detrimental in building one’s retirement nest. Thankfully, we have the choice to switch over to the new system or stay in the old one.

Individuals can choose to pay taxes at lower rates if they forego the deductions and exemptions available to them. Depending on how much one avails of these deductions, he will be left with greater liquidity even if he doesn’t invest in chapter VI A Deductions, by paying almost similar taxes, which a person would pay in the existing tax structure should he avail all deductions and exemptions.

Individuals earning between Rs 10-15 lakhs and not investing in 80C investments or are covered by their corporate medical policy and don’t have their own Mediclaim or home loans, will benefit with the new rates. Individuals with higher incomes will not benefit if they forego the exemptions and move to new tax regime.

Mutual Fund Investors: As per the new proposal, dividends distributed by MF will be subject to 10% TDS. Later CBDT issued a clarification that the TDS @ 10% will apply only to Dividend payments and not applicable on capital gains arising at the time of redemption of units of a MF.

Bank Fixed Deposit Holder: Deposit Insurance and Credit Guarantee Corporation has been permitted to increase deposit insurance coverage for a depositor from existing Rs. 1 Lakh to Rs. 5 Lakhs. This move will comfort small depositors and senior citizens, who keep their savings in banks for monthly cash flow.

Bond/G Sec ETF: The Government has proposed a Debt ETF consisting of Govt. Securities, which gives retail investors access to government securities. This was done after the recent success of the Bharat Bond ETF.

- Myths And Facts About Therapy - 18 June2022

- Nominee V/s Legal Heir: Who Wins? - 18 September2021

- Importance Of Successive Nomination During The Pandemic - 19 June2021