Khushroo B. Panthaky is a Chartered Accountant and a Senior Partner with 38 years of experience in an Accounting and Audit firm.

The Budget 2023 lays emphasis on economic growth through capital expenditure, all-round inclusive development, supportive business environment, reduced compliance burden and reduction in the tax outgo for individual taxpayers opting for the new tax regime. It also sends a strong signal to the global investment and business community by reiterating the government’s position on restricting the fiscal deficit, which is expected to be brought down to below 4.5% by 2025-26, from the current 6.4%.

Proposals Under Union Budget 2023: Impact On Individuals

Select key changes impacting individual taxpayers are summarized hereunder:

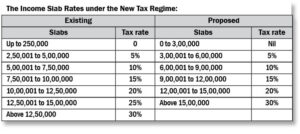

Changes In New Tax Regime: The new tax regime is proposed to be treated as the default tax regime. However, taxpayers would continue to have the option to select the old tax regime.

- Resident individuals will be entitled to 100% rebate of the amount of income-tax payable on total income not exceeding INR 7 lakhs. Hence, resident individuals earning INR 7 lakhs or less will not pay any tax under the new tax regime.

- Standard deduction of INR 50,000 and deduction for family pension (1/3rd of pension or INR 15,000, whichever is less) are also proposed under the new tax regime.

- Presently, the rate of surcharge on income exceeding INR 5 crore is high at 37%, which means an effective tax rate of 42.74%. This rate is proposed to be reduced to 25% under the new tax regime.

Overall, the tax outflow of middle-class taxpayers and High Net-Worth Individuals are expected to reduce under the proposed new tax regime. However, an evaluation needs to be done on a case-to-case basis, as many other exemptions/deductions that are otherwise allowed under the old regime, like House Rent Allowance, Leave Travel Allowance, Interest on housing loan, etc., are not available under the new regime.

Life Insurance Policies: The Budget 2023 proposes to tax income received from Life Insurance Policies issued on or after 1 April, 2023, in case the aggregate annual premium exceeds INR 5 lakh, except when received on death of the assured. This reduces the attractiveness of life insurance as an investment avenue for High-Net-Worth Individuals (HNIs). However, Term plans offered by the insurance companies may gain further traction.

Tax Collection At Source (TCS) on Foreign Remittances Made Under LRS: It is proposed to increase the TCS rate from 5% to 20% on foreign remittances by resident individuals under the Liberalised Remittance Scheme, without any threshold, excluding remittances for education and medical treatment. Individuals can claim such TCS against their taxes payable for the relevant tax year. However, the same may have an impact on the immediate cash flows of the individual.

Increase In Exemption Limit For Leave Encashment: The budget proposes to raise the exemption limit for leave encashment received upon retirement by non-government salaried employees to INR 25 lakh from the current INR 3 lakh. This is a welcome change mentioned in the Budget speech, but a separate notification is awaited.

Capital Gains Deduction On Purchase Of Residential Property: Deduction from capital gains on reinvestment in new residential property is currently available to individuals and HUFs, without any monetary limit. The deduction is now proposed to be capped at INR 10 crore. This proposal can significantly impact High Net-worth Individuals planning to invest in luxurious properties in the future.

Taxation Of Capital Gains In Case Of Market-Linked Debentures: Long-term capital gains arising from market-linked debentures (MLDs) are currently taxed at a concessional rate of 10%. It is proposed to tax such gains as short-term capital gains at normal rates. The rationale for the proposed increase in tax is that MLDs are in the nature of derivatives, which are normally taxed at applicable rates and not at a concessional rate.

Capital Gains Exemption On The Conversion Of Gold To EGR: Conversion of gold into EGR or Electronic Gold Receipts, (issued by a vault manager) or vice versa is proposed to be exempt from capital gains tax.

Most of the above changes are applicable from Assessment Year 2024-25 onwards. These are proposed changes and the Bill will become law, once approved by the Hon’ble President. Overall, the Union Budget is appreciated by the industry and the individuals and would be remembered for a long time as a landmark budget.

- મા તે મા બીજા વગડાના વા - 11 May2024

- સુધારેલ એસ ડી મોદી પારસી ગર્લ્સ હોસ્ટેલ ફરી ખુલ્યું - 11 May2024

- શ્રીજી પાક ઈરાનશાહ આતશબેહરામની 1304મી સાલગ્રેહની ઉજવણી કરવામાં આવી - 11 May2024