Khushroo B. Panthaky

Finance Bill, 2025, clearly outlines adequate thrust on accelerated economic growth, a surge in investments in the private sector, a greater transparency, and positioning India at a higher level globally. The four growth-engines identified by the Hon’ble Finance Minister – Agriculture, Micro Small and Medium Enterprises (MSMEs), Investments and Exports – would drive India to become one of the strongest global economies. It lays down a distinct emphasis on the “middle-class” and looks to reinforce the trust of taxpayers. Numerous amendments for the middle class are included in existing schemes like UDAN (Ude Desh ka Aam Aadmi) which boosts regional connectivity, and SWAMIH (Special Window for Affordable and Mid-Income Housing), which eases the burden of EMIs and rent. The Bill also emphases enhancing the spending power of middle-class through amendments in personal income tax (discussed below) – a key priority.

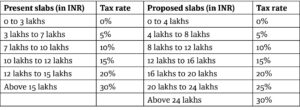

Changes In New Tax Regime: The Finance Bill 2025 has once again proposed changes to the existing income-tax structure for individual taxpayers, to aid in boosting household consumption, savings and investment, as under:

Rebate: It is also proposed to increase the rebate under the new tax regime from INR 7 lakhs to INR 12 lakhs. Thus, those who earlier paid a tax of Rs. 80,000 on income of Rs. 12 lakhs will now pay Nil tax. Similarly, those with income of Rs.25 lakhs shall get benefit of Rs.10 lakhs via tax savings. This is only available to resident individuals.

Marginal Relief: It is proposed to provide marginal relief where the tax payable by an individual on the amount of total income exceeding INR 12 lakhs is more than the amount that exceeds INR 12 lakhs. To illustrate, in the absence of marginal relief, a person having an income of INR 12.10 lakhs, shall pay tax of INR 61,500 (5% of INR 4 lakhs + 10% of INR 4 lakhs and 15% of INR 10,000). However, due to marginal relief, the amount of tax shall be INR 10,000, i.e., marginal relief of INR 51,500 shall be available (INR 61,500 – INR 10,000). It is critical to note that this is also available only to resident individuals.

Taxation of Unit Linked Investment Plan (ULIP): Presently, the amount received under a ULIP is exempt, provided that the premium paid does not exceed INR 2.5 lakhs. It is now proposed that all ULIPs which are not eligible for exemption would be treated as capital asset and profits from its redemption would be taxable as capital gains. These provisions would be applicable with effect from (w.e.f) Assessment Year (AY) 2026-27.

Determining Annual Value Of Self-Occupied Property: Presently, the taxable annual value for two self-occupied house properties can be claimed as ‘Nil’ if the owner has occupied the house, or the owner could not occupy it due to his employment, business, or profession continuing at another place. The Bill now proposes to extend an unconditional benefit of treating the annual value of 2 self-occupied properties as Nil, thus even when property cannot be occupied, the annual value of 2 properties can be considered as Nil. This would be applicable w.e.f. AY 2025-26, thereby providing a fantastic opportunity to those who may wish to divert their savings into an additional housing property.

Tax Benefits On Contribution To NPS Vatsalya: Though NPS Vatsalya was introduced vide Finance Act, 2024, no tax benefit was provided for contribution towards the fund. It has been proposed that parents / guardians can claim tax deduction of up to Rs. 50,000 annually for the amount deposited in the NPS Vatsalya account, for up to two children under the old tax regime. Such deduction would be within the overall limit of Rs. 50,000 specified for regular NPS. These provisions would be applicable w.e.f. AY 2026-27.

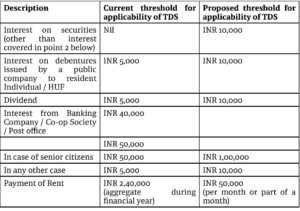

CHANGES IN TAX DEDUCTED AT SOURCE (TDS) AND TAX COLLECTION AT SOURCE (TCS)

TDS: The Bill provides an increased threshold for specified payments on which TDS is applicable, some of which are hereunder:

TCS: The threshold of INR 7 lakhs has been proposed to be increased to INR 10 lakhs for remittance under Liberalised Remittance Scheme (LRS), other than remittance for the purpose of education, financed by a loan from a specified financial institution. Further, where remittance under LRS is for the purpose of education which is financed by a loan from a financial institution, then no TCS shall be applicable.

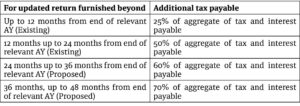

Updated Income-Tax Return: Time-limit for filing updated return is proposed to be increased from 24 months to 48 months from the end of the relevant Assessment Year (AY). However, such delays result in payment of additional tax, discussed as under:

In conclusion, the Union Budget 2025 supports consumption in the backdrop of elevated inflation and muted wage growth, which had eroded the purchasing power of people. Budget 2025 also provides for lower tax outflow, thus an increase in disposable income which can enhance the standard of living. Overall, the Budget has been well received by individual tax payers. The granular impact of the new tax bill on individuals remains to be seen.

- સોરાબજી બરજોરજી ગાર્ડા કોલેજ ટ્રસ્ટ, નવસારી - 8 February2025

- અજમલગઢ ખાતે ઐતિહાસિક જશન યોજાશે - 8 February2025

- સાહેર અગિયારીએ 179મા સાલગ્રેહનીભવ્ય રીતે ઉજવણી કરી - 8 February2025