An FD is a financial investment option offered by banks which provides investors (bank account holders) with a higher rate of interest, than a regular savings account. It has fixed tenures – ranging from investing an amount for a few months to years. FDs don’t have fancy returns but serve the purpose of preserving capital which is most important for some people. In India, total FDs amount to over Rs. 75,000 Billion, as per the Reserve Bank Of India.

Pros of an FD:

- FDs give a stable and fixed monthly income on the money invested. The interest rate is fixed during the tenure of the FD.

- It is for the safety of principal that attracts most of the investors to opt for FD’s. The capital (upto 1 lakh) has the highest safety compared to any other debt investment as it is guaranteed by Deposit Insurance And Credit Scheme Of India.

- FDs are considered to be highly liquid assets as they can be liquidated within minutes with online withdrawal facilities.

- Many banks give credit against FD and charge about 2% on the loan facility extended against the FD.

Cons of an FD:

FDs are fully taxable. The interest is taxed at the investor’s marginal tax rate.

With FDs, you can’t generate inflation-beating real returns. The real returns after adjusting for inflation is either NIL or negative for investors in higher tax bracket.

Now let’s understand Mutual Funds. These are investments made in the debt market, funded by shareholders, that trade in diversified holdings and are professionally managed. MFs offer investors the opportunity to take exposure in debt securities and money markets through debt funds, which otherwise remain inaccessible to retail investors. Equity MFs are ideal for long term investment and wealth creation, while debt funds are ideal for short term investments (upto 3 years) with a conservative risk profile.

Pros of MFs:

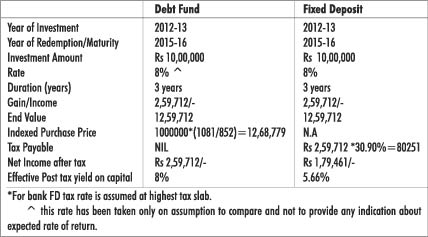

- If debt funds are held for more than three years, they qualify for long term capital gains and enjoy indexation benefit. (refer to the chart)

- No TDS is deducted on debt funds redemptions.

Cons of MFs:

- The returns under debt funds are not assured and are dependent on interest rate movements in the economy. Market price of debt securities are inversely related with interest rate movements.

The fact is that debt schemes and FDs are two different species under the same asset class. While in FD, interest income is guaranteed, there is no scope for any appreciation. On the other hand, debt schemes are relatively riskier than FDs and the returns are not guaranteed. But the tax benefits enjoyed by debt funds make them better investment options than FDs for investors in the higher tax bracket.

- સુનાવાલા અગિયારી ખાતે આવાં અર્દવિસુર પરબ - 27 April2024

- XYZ ‘Cook Off 2024’ – A Delicious Success! - 27 April2024

- Boman Irani Celebrates ‘Spiral Bound’s 700 Sessions Milestone - 27 April2024