Marzee Kerawala is a Certified Financial Planner with expertise in Income Tax and Investment products. Managing assets worth over Rs. 4 Billion, his firm ‘NiveshIndia’, designs Tailored Investment Strategy through Customised Financial Planning for individuals and NRIs, and also handles Treasury Management for corporates and SMEs. You can contact him at +91 9987567667 or Email: marzeek@niveshindia.co.in [Website is www.niveshindia.in]

As Investors, we like to think that every decision to buy or sell a particular investment has a logic to it. Unfortunately, that’s not always the case. As investors, we are inherently vulnerable to biases that lead us to illogical and irrational investment decisions; Biases are part of human behavior and we are prone to be misled. Most times we are not even aware that we suffer from these biases.

In my last article I had elaborated on ‘Mental Accounting Bias’ while investing. In this column we will discuss ‘Recency Bias’ with real life examples. It is a behavioral bias wherein there is tendency to weigh recent/current events more heavily than earlier events. Investors put all their emphasis on recent happenings and give less weightage to those that have happened in past, thus shifting the focus towards the asset class which is the flavor of the day.

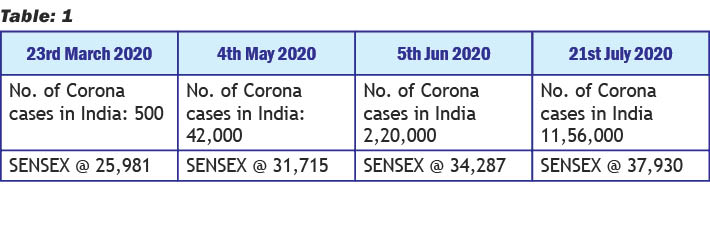

This skews perception towards short term thinking. We have seen many such events in India where investors either tend to be overweight or underweight on the asset class. Few recent events in Indian context are mentioned below:

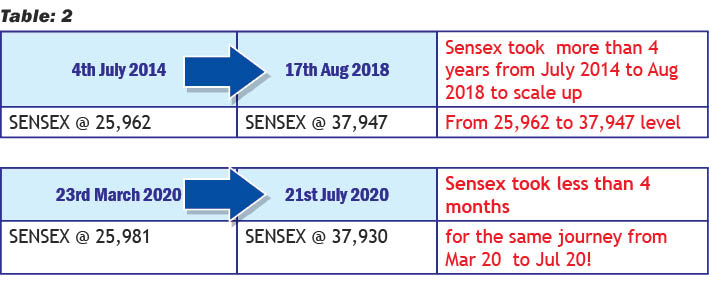

Upon taking a closer look at the above tables, it’s clear that the Sensex had hit the lows of 26K by Mar 2020 when the corona cases in India were less than 500! Most people extrapolated this bad news and sold their equities (not that I am trying to justify these 38K level on index). We can see that when the markets were crashing in March 2020 due to Covid-19, risk aversion increased and people sold their equity holdings and moved to the safety of FDs or Gold. Risk appetite dries up as the future looks hopeless due to the developments of lockdown and contracting GDP. The same holds true during the bull markets, risk appetite normally increases and they extrapolate the recent equity gains into the future. It clearly shows that Investors who sold their equity at the depths of Mar 2020 and moved to Fixed Deposits are shocked to see Sensex back again @ 38000!

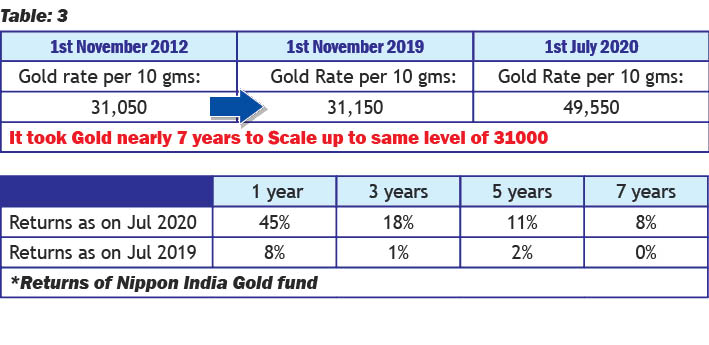

*Returns of Nippon India Gold fund

If you look at the gold prices, they also show a similar trend. Between November 2012 to November 2019, gold prices were almost the same @ Rs. 31,000. For an investor who has invested in gold, there has effectively been zero returns in this asset class for 7 years! So, if you had invested in gold and seen the gold returns as on July 2019 a year back, the returns for 3, 5 and 7 years were 1%; 2%; and 0% CAGR respectively!

The same gold delivered 45% returns in the last one year and, as recently as July 20, the returns for 3, 5 and 7 years are 18%; 11% and 8% CAGR respectively. Those investors who shunned this asset after getting frustrated for 7 years with zero returns are also shocked to see gold @ 49,500. In both the above examples, Recency Bias led investors to make these irrational decisions.

But here’s the good news! Evidence suggests that if we become aware of our biases, we can also learn to overcome them and improve our decision making. So how can we deal with this bias? First of all, acknowledge it. Half the battle is won when you identify its presence – that it, in fact, has been existing all this time! Don’t be hard on yourself – many investors fall prey to it.

We need to work on what is in our control – Asset Allocation, Diversification, and setting realistic expectation from our investments. Don’t get swayed by the latest performance, however good or bad. At finally and most importantly, get yourself professional assistance. The services of a Financial Advisor are essential to set you sailing in turbulent market conditions!

- Myths And Facts About Therapy - 18 June2022

- Nominee V/s Legal Heir: Who Wins? - 18 September2021

- Importance Of Successive Nomination During The Pandemic - 19 June2021